|

Financial pros searched Tesla (TSLA) nearly six times more than the next closest stock this past month, according to our TrackStar data.

The reason is obvious. Tesla reported Q1 2026 earnings Wednesday, beating on both EPS and revenue.

Shares jumped 4% in after-hours trading. Then the company told investors it would spend $25 billion in capex this year, up from prior guidance of $20 billion. The stock gave it all back.

That whipsaw reaction tells you everything about where Tesla stands today. It's not a car company anymore, at least not in its own mind. But the car business still pays the bills, and right now, those bills are getting bigger.

Here's whether the AI story justifies the price.

Tesla's Business

Founded in 2003 and led by Elon Musk since 2008, Tesla spent its first decade proving electric vehicles could be desirable. It spent the next decade proving they could be profitable. Now it's trying to prove it can be something else entirely.

Tesla designs, manufactures, and sells electric vehicles, energy storage systems, and solar products. It also develops autonomous driving software and humanoid robots, a combination no other automaker has attempted at scale.

Tesla segments its business into the following areas:

- Automotive (72% of total revenues) - Vehicle sales, leasing, regulatory credits, and FSD software

- Energy Generation and Storage (11% of total revenues) - Megapack battery systems and solar products

- Services and Other (17% of total revenues) - Supercharging, vehicle repairs, insurance, and used car sales

Q1 2026 revenue rose 16% year-over-year to $22.4 billion, beating expectations. Non-GAAP EPS came in at $0.41 versus the $0.37 consensus. But a closer look reveals some uncomfortable details.

Energy revenue fell 12% year-over-year to $2.4 billion. The quarter also benefited from one-time warranty and tariff adjustments that management acknowledged on the call.

The bigger story is what Tesla is building toward. Paid Robotaxi miles nearly doubled sequentially in Q1. The service launched in Dallas and Houston in April. FSD received regulatory approval in the Netherlands, the first EU country, clearing a path for broader European expansion.

Tesla also completed the final chip design of its next-generation AI5 inference processor and is partnering with SpaceX to build what it calls the largest chip fabrication facility ever attempted. Preparations for a large-scale Optimus robot factory begin in Q2, with a long-term target of one million units per year.

These are moonshots. Musk has missed timelines before. But the infrastructure investment is real and accelerating.

Financials

Source: Stock Analysis

Tesla generated $97.9 billion in trailing twelve-month revenue, up just 2.3% year-over-year. That's a dramatic deceleration from the 18.8% growth posted in FY2023 and the 51% growth in FY2022.

Gross margin sits at 19.1% on a TTM basis, an improvement from the 17.9% reported last year. Operating income of $4.9 billion reflects a 5.0% operating margin, thin for a company trading at this valuation.

Operating cash flow came in at $3.9 billion for Q1 alone, a strong quarter. TTM free cash flow stands at $7.0 billion, up 12.5% from the prior period.

That's the good news. The bad news is that Tesla just guided $25 billion in capex for the full year. At that pace, free cash flow will compress significantly in coming quarters.

The balance sheet holds approximately $17.7 billion in cash and short-term investments, which provides a buffer. But a $25 billion annual capex commitment is a serious bet for a company generating $7 billion in annual free cash flow.

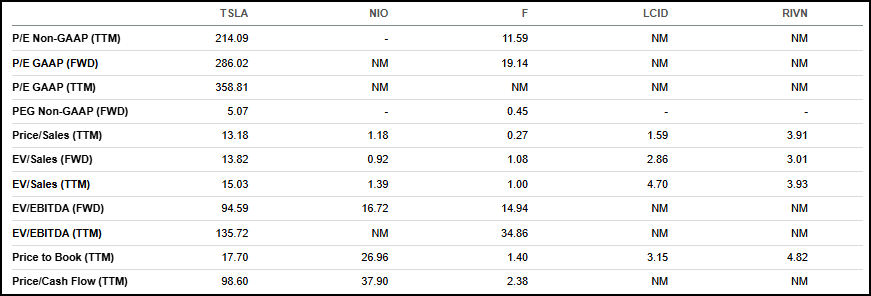

Valuation

Source: Seeking Alpha

There is no gentle way to say this. Tesla trades at 214x trailing non-GAAP earnings. Ford (F) trades at 11.6x. Even on price-to-sales, Tesla commands a 13.2x multiple versus Ford's 0.3x.

Price-to-cash-flow tells the same story. Tesla trades at 98.6x, compared to Ford at 2.4x and NIO (NIO) at 37.9x.

None of this is new. Tesla has always carried a premium. The question is whether the Robotaxi and Optimus narratives can eventually grow into that valuation, or whether the stock is simply pricing in a future that may never arrive on time.

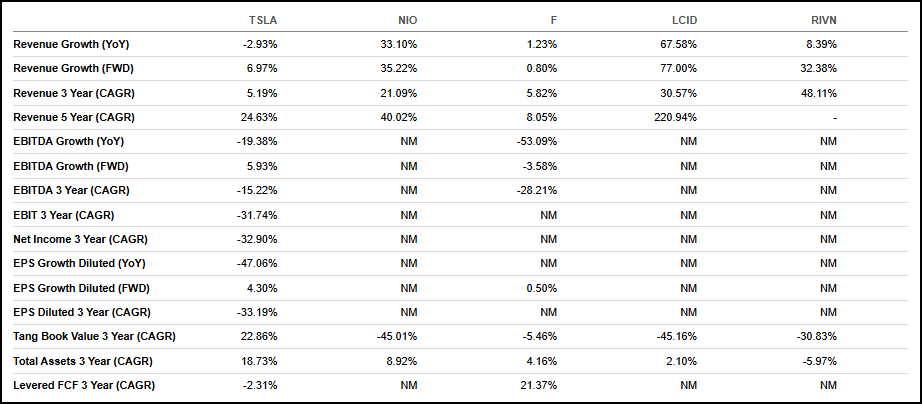

Growth

Source: Seeking Alpha

Tesla's forward revenue growth estimate sits at 7.0%, respectable for an automaker but modest for a company priced like a high-growth tech stock.

EPS growth on a TTM basis is down 37.4%. FCF growth over three years is negative 2.3% on a CAGR basis.

Peers like Rivian (RIVN) and Lucid (LCID) post higher revenue growth rates, but from bases so small the comparisons are nearly meaningless. Ford shows 1.2% revenue growth, making Tesla look dynamic by comparison.

The honest assessment is that Tesla's core growth engine stalled. The new growth engines -- Robotaxi, Optimus, energy storage -- are still early innings.

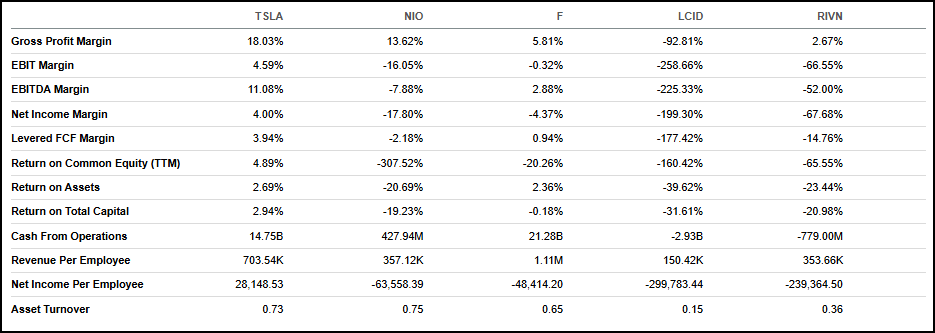

Profitability

Source: Seeking Alpha

Tesla leads this peer group on every profitability metric that matters.

Gross margin of 18.0% is well ahead of Ford's 5.8%, NIO's 13.6%, and Rivian's (RIVN) 2.7%. EBIT margin of 4.6% and levered FCF margin of 3.9% are the only positive figures in the group outside of Ford's thin FCF margin.

Cash from operations of $14.8 billion on a TTM basis dwarfs the competition. Revenue per employee of $703,540 is nearly double NIO's figure.

Tesla is a profitable company in a sea of money-losers. That distinction matters, even if the valuation doesn't reflect it proportionally.

1.5 Million Users Onboard This Pre-IPO CompanyImmersed stands out for one big reason: people already rely on it to do their jobs. - 1.5M+ professionals onboarded to date - Users spend 40–60 hours per week working inside it - #1 productivity app in the Meta Quest ecosystem - Partnerships with Meta, Google, Intel, and Qualcomm - Reserved NASDAQ ticker: $IMRS - Early investors qualify for up to 20% bonus shares Access Pre-IPO pricing at $0.72 per share, before public markets weigh in. Invest Before the Pre-IPO Round Closes[Ad]

Our Opinion 6/10

Tesla is a genuinely profitable, cash-generating business with technology assets no other automaker can match. The Robotaxi expansion, FSD progress, and Optimus ambitions represent real optionality.

But 214x earnings prices in an enormous amount of success that hasn't materialized yet. A $25 billion capex commitment will pressure free cash flow for years. Core auto revenue growth has slowed sharply, and consumer backlash tied to Musk's political activity remains a headwind in key markets.

The stock suits investors with a long time horizon and tolerance for volatility. For everyone else, the risk-reward doesn't add up at this price.

|