|

Markets are rattled. The U.S.-Iran conflict has sent oil prices climbing, rattled supply chains, and left investors scrambling for cover.

Coca-Cola (KO) stock is up roughly 11% year-to-date, outpacing the broader consumer staples sector as investors have re-rated it as a defensive hold.

Then Q1 earnings dropped this morning — and the stock popped.

Search volume by financial pros hit 5,201 this past month, nearly 38% more than runner-up PepsiCo, according to our TrackStar data.

The question now: is the safe-haven premium justified, or is this just a flight-to-quality trade running out of runway?

Coca-Cola's Business

The Coca-Cola Company has spent over 130 years building what may be the most recognized brand on earth. What sets it apart isn't the formula — it's the system: a vast global network of bottling partners reaching more than 200 countries and territories with minimal capital intensity at the parent level.

The company operates primarily as a brand and concentrate manufacturer, not a bottler.

That model keeps margins high and capital requirements low, with roughly 700,000 people employed across the entire Coca-Cola system worldwide.

Coca-Cola segments its business into the following areas:

- Europe, Middle East & Africa (EMEA) (24% of revenues) - Beverages including sparkling soft drinks, water, and tea across a diverse mix of developed and emerging markets

- North America (39% of revenues) - The company's largest and most profitable region, serving consumers through retail, food service, and convenience channels

- Latin America (13% of revenues) - High-growth markets with strong Trademark Coca-Cola and Sprite brand presence

- Asia Pacific (12% of revenues) - Developing markets including China and India, with significant long-term volume runway

- Bottling Investments (13% of revenues) - Consolidated bottling operations primarily in markets being prepared for refranchising

Q1 2026 marked the first quarterly report under new CEO Henrique Braun.

Net revenues grew 12% to $12.5 billion, and organic revenues grew 10%, driven by an 8% increase in concentrate sales and 2% growth in price/mix. Comparable EPS grew 18% to $0.86, beating analyst estimates of $0.81.

Coca-Cola Zero Sugar was the standout, posting 13% volume growth globally across every geographic segment.

The one soft spot: juice, value-added dairy, and plant-based beverages declined 1% in volume, as growth in fairlife and Santa Clara couldn't offset the exit from Nigeria.

The company raised its full-year comparable EPS growth outlook to 8%-9%, up from 7%-8%, while maintaining organic revenue growth guidance of 4%-5%. Management noted that while commodity volatility from the Middle East conflict is worth watching, the overall impact on costs remains manageable.

The company is also leaning into AI-driven marketing. A Chinese New Year campaign used AI-generated consumer portraits tied to connected packaging.

During March Madness, Coca-Cola and BODYARMOR activated a "Fan Work is Thirsty Work" platform across the Men's Final Four. These aren't one-offs — they reflect a broader push to deepen consumer connections through culturally relevant, data-informed campaigns.

Financials

Source: Stock Analysis

Coca-Cola's financial profile is exactly what you'd expect from a Dividend King: consistent, high-margin, and cash generative.

TTM revenues stand at $49.3 billion, up 5.1% year over year. Gross margins are running at 61.7% on a TTM basis, and operating margins have expanded to 29.3% — well ahead of 2023 and 2024 levels.

Free cash flow tells the most important story. TTM free cash flow reached $12.6 billion, up 137.2% from the prior year, driven partly by the completion of the fairlife contingent consideration payment in 2025. Management guides for $12.2 billion in full-year 2026 free cash flow.

The balance sheet carries $43.9 billion in gross debt against $13.8 billion in total cash and securities, leaving net debt of $30.1 billion. Net debt leverage sits at a manageable 1.6x comparable EBITDA. The dividend costs roughly $8.8 billion annually and has grown for 63 consecutive years.

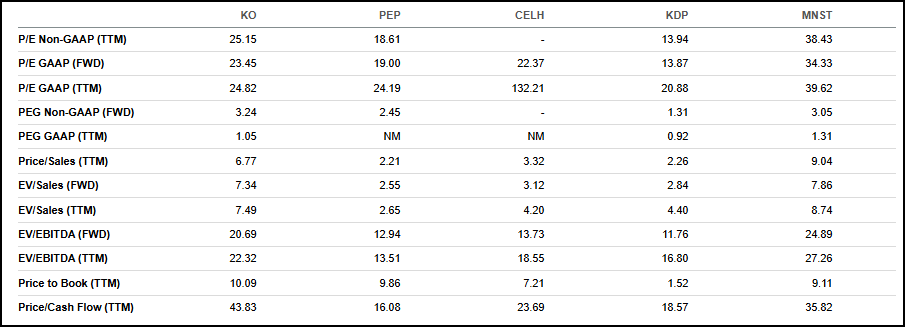

Valuation

Source: Seeking Alpha

At 25.2x trailing non-GAAP earnings and 43.8x price-to-cash flow, Coca-Cola is the premium name in this peer group. Keurig Dr Pepper (KDP) trades at just 13.9x non-GAAP earnings and 18.6x cash flow, while PepsiCo (PEP) sits at 18.6x and 16.1x respectively.

Monster Beverage (MNST) commands a higher P/E at 38.4x but trails KO on most other measures. The premium Coca-Cola carries reflects its brand durability and capital-light model — though it does limit upside at current prices.

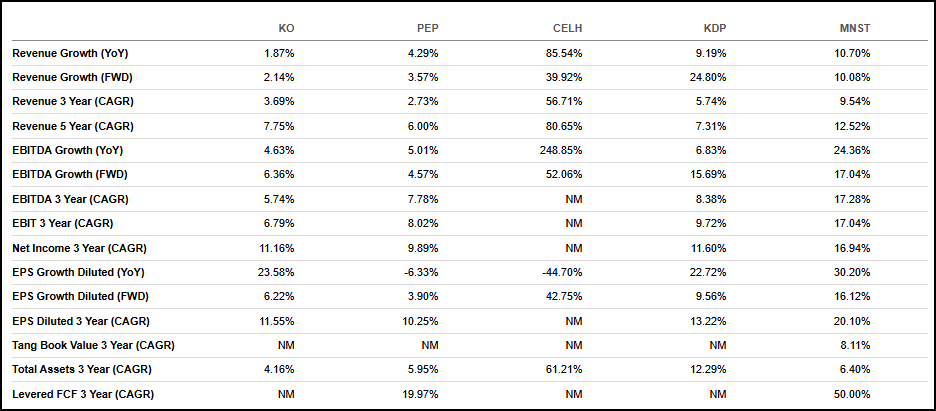

Growth

Source: Seeking Alpha

Coca-Cola's 1.9% trailing revenue growth trails the peer group. Celsius Holdings (CELH) leads with 85.5%, while KDP sits at 9.2% and MNST at 10.7%.

On a 3-year CAGR basis, KO's 3.7% is the weakest of the group. EPS diluted growth of 23.6% on a trailing basis is the standout, reflecting margin improvement and a lower tax rate. Forward revenue growth of 2.1% is modest, though forward EPS growth of 6.2% is more competitive.

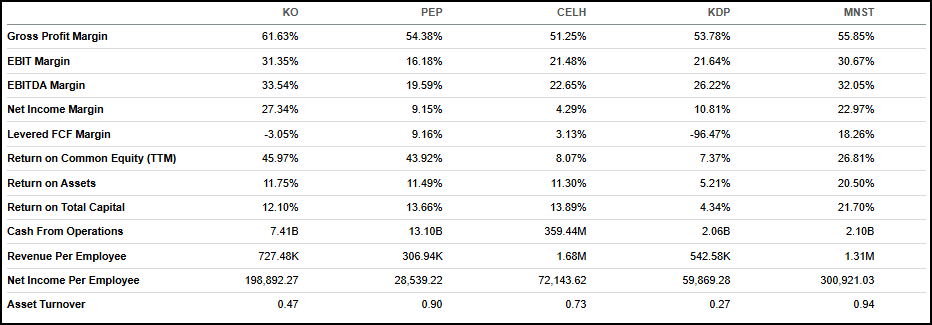

Profitability

Source: Seeking Alpha

This is where Coca-Cola separates itself. A 61.6% gross profit margin leads the peer group. Its EBIT margin of 31.4% is nearly double PepsiCo's 16.2% and well ahead of KDP's 21.6%. Return on equity stands at 46.0% — the highest in the group.

Return on assets of 11.8% is also best-in-class. Cash from operations of $7.4 billion trails only PepsiCo's $13.1 billion in absolute terms.

The one blemish: a levered free cash flow margin of -3.1%, which is distorted by the timing of cash payments and not reflective of the underlying business strength.

[URGENT] Wall Street is hiding this from youThe current economic chaos is just a preview … What's coming next could be way scarier. That's according to a strange investment secret - discovered just before the Great Depression … And it's likely to catch most Americans by surprise. If you're retired or planning to retire … If you have any kind of money in the stock market … Click here to learn more - before it's too late![Ad]

Our Opinion 8/10

Coca-Cola isn't a growth story. It never was. But right now, it's exactly the kind of stock investors want to own.

The business model is capital-light, globally diversified, and remarkably resilient. The new CEO is off to a strong start, and raised EPS guidance signals management confidence even as the macro environment grows more uncertain.

At 25x earnings, you're paying a premium. But you're getting 63 years of dividend growth, a fortress brand, and $12+ billion in annual free cash flow in return.

For long-term investors, this remains a core holding.

|