|

For the first time in over a decade, Verizon (VZ) added postpaid phone subscribers in Q1.

That's not a small thing. Verizon spent years bleeding customers to T-Mobile (TMUS) while its stock went nowhere.

New CEO Dan Schulman took the helm with a simple mandate: stop the bleeding, then grow. Q1 2026 suggests the plan is working.

Search volume from financial pros hit 5,200 in the past month, according to our TrackStar data. That's nearly 70% more than AT&T (T), the second most searched name in telecom.

So what's driving the interest? And more importantly, does the stock deserve a spot in your portfolio?

Here's what we found.

Verizon's Business

Verizon Communications is America's largest wireless carrier by revenue, with a network that blankets over 146 million retail connections nationwide. The company built its reputation on network reliability, and that reputation still drives customer decisions today.

Verizon serves consumers, businesses, and government clients through wireless and wireline services. Its recent $20 billion acquisition of Frontier Communications added significant fiber broadband scale, pushing total broadband connections to 16.8 million.

Verizon segments its business into the following areas:

- Consumer (approx. 75% of total revenues) - Includes mobility and broadband services sold to individual and household customers, encompassing postpaid, prepaid, and fixed wireless products

- Business (approx. 25% of total revenues) - Provides wireless, wireline, and networking solutions to enterprise, mid-market, and government clients

- Other - Includes legacy wireline products and miscellaneous revenue streams

Q1 2026 marked a genuine inflection point. Verizon posted 55,000 net postpaid phone additions, the first positive Q1 result since 2013. Adjusted EBITDA hit a company record of $13.4 billion, up 6.7% year over year. Adjusted EPS came in at $1.28, up 7.6%.

Schulman has been relentless about reducing friction for customers. Churn fell to 0.90%, down 5 basis points sequentially. That's the kind of operational improvement that compounds over time.

The Frontier acquisition, closed in January 2026, is central to the long-term growth plan. Fiber is a stickier, higher-margin product than legacy copper, and Verizon now has the footprint to compete aggressively in home broadband.

Management raised full-year guidance on adjusted EPS to $4.95-$4.99 and expects postpaid phone net adds to land in the top half of its 750,000 to 1 million target range.

Financials

Source: Stock Analysis

Verizon's TTM revenue reached $139.1 billion, up 2.9% year over year. That's modest growth, but it represents an acceleration from the flat-to-declining trend of the prior three years.

Operating cash flow came in at $8.0 billion in Q1 alone, with free cash flow of $3.8 billion after $4.2 billion in capital expenditures. The dividend costs $2.9 billion per quarter, which free cash flow covers. Verizon also resumed share buybacks, spending $2.5 billion in Q1.

The balance sheet is the main concern. Total debt surged to $172.5 billion following the Frontier deal, with net unsecured debt to adjusted EBITDA at 2.6x.

Management has guided for $21.5 billion or more in full-year free cash flow, which should help reduce leverage over time. It's manageable, but it limits flexibility.

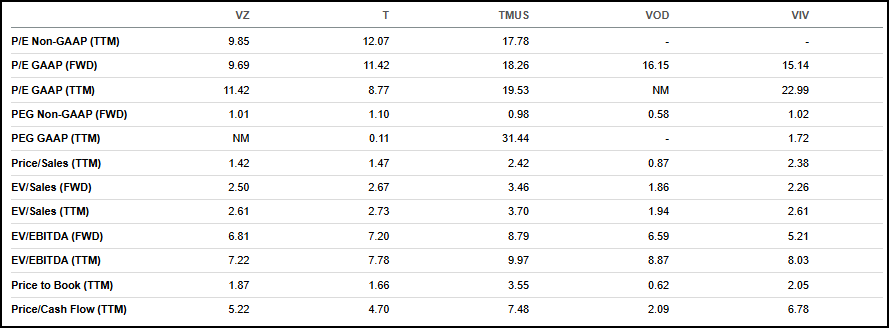

Valuation

Source: Seeking Alpha

Verizon is the cheapest name in its peer group by almost every measure. It trades at 9.7x forward earnings and just 5.2x price to cash flow. T-Mobile trades at 18.3x forward P/E and 7.5x cash flow. AT&T sits in the middle at 11.4x forward P/E and 4.7x cash flow.

For investors willing to accept slower growth, Verizon offers a compelling entry point relative to its peers.

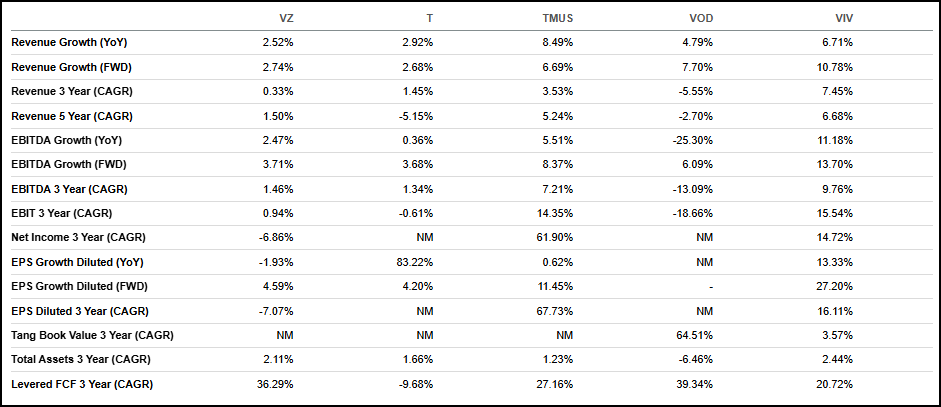

Growth

Source: Seeking Alpha

This is where Verizon's story gets complicated. Revenue growth is 2.5% year over year, and the three-year CAGR is just 0.3%. T-Mobile runs a 3.5% three-year revenue CAGR while also putting up 61.9% net income growth over three years. Verizon's net income three-year CAGR is -6.9%.

The bright spot is free cash flow. Verizon's levered FCF three-year CAGR of 36.3% leads the entire group. If management executes on Frontier integration and fiber expansion, the revenue line should improve in 2027 and beyond.

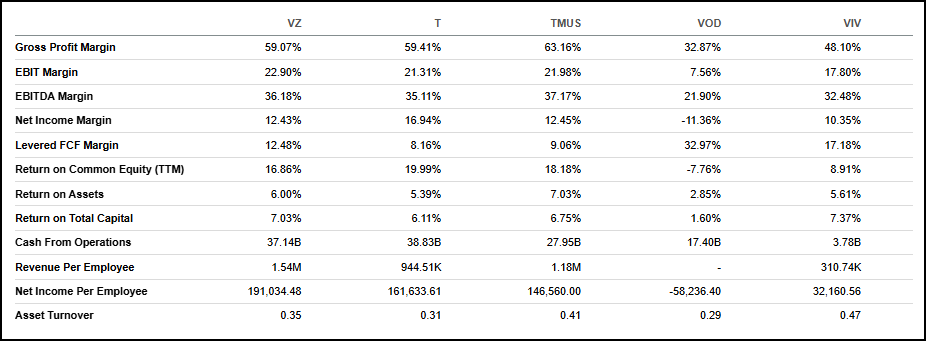

Profitability

Source: Seeking Alpha

Verizon's gross margin sits at 59.1%, essentially in line with AT&T's 59.4% but behind T-Mobile's 63.2%. EBIT margin of 22.9% is the strongest in the group. Net income margin of 12.4% trails AT&T's 16.9%, partly due to higher interest costs from the debt load.

The standout figure is cash from operations at $37.1 billion TTM, the highest among peers. That raw cash generation is what keeps the dividend safe and funds the buyback program.

Next for Nvidia: $10 TrillionNvidia has already established itself as an AI powerhouse. Its chips, platforms and AI roadmap have already positioned it to dominate AI for the near future. But Nvidia is not standing pat. It's not waiting for other companies to catch up to its revolutionary technology. Instead, Nvidia CEO Jensen Huang is moving on to the next frontier for Nvidia to conquer. He calls them AI factories. And every tech titan — Amazon, Google, Microsoft and Meta — all desperately need them. Guess who will be deeply involved in the buildout of these massive superstructures! That's right. Nvidia. And thanks to these AI factories, Nvidia is on a beeline to becoming a $10 trillion company by 2030, if not sooner. To learn more about this massive prediction, click here[Ad]

Our Opinion 7/10

Verizon isn't a growth stock. But it doesn't need to be.

The turnaround under Schulman is real and measurable. Postpaid adds are positive, churn is falling, EBITDA is at record levels, and free cash flow is accelerating. The Frontier deal adds long-term fiber optionality.

The debt load is elevated and growth will remain modest for the foreseeable future. T-Mobile will continue to outpace Verizon on subscriber momentum.

For income-oriented investors, a stock yielding close to 6% with rising free cash flow and a decade of dividend increases is hard to dismiss. This is a buy for patient investors, not a trade.

|