|

Robinhood pulled in nearly four times the search interest of any other broker on our list this month.

That's not a typo. Robinhood Markets (HOOD) drew 6,997 searches from financial pros while Morgan Stanley managed 1,777.

The catalyst arrived April 28 when Robinhood reported Q1 2026 earnings. Revenue grew 15% to $1.07 billion. EPS rose 3% to $0.38. Both numbers missed Wall Street's targets.

Shares slipped roughly 3% premarket the next morning.

Yet underneath the miss sat a long list of records: 4.3 million Gold subscribers, $307 billion in platform assets, and a 320% surge in event contracts revenue.

So is this a buying opportunity or a warning shot? Here's our take.

Robinhood's Business

Robinhood operates a commission-free trading platform that broke open retail investing for a generation that grew up on smartphones. The company now describes itself as a global financial super app, blending brokerage, crypto, banking, and private markets access.

The platform serves 27.4 million funded customers across equities, options, futures, crypto, and prediction markets. Robinhood Gold, the premium tier, just crossed 4.3 million subscribers, a 36% jump year over year.

Robinhood segments its business into the following areas:

- Transaction-based revenues (58% of total) - Fees from options, equities, crypto, and event contracts trading

- Net interest revenues (34% of total) - Interest earned on margin loans, cash sweep, and securities lending

- Other revenues (8% of total) - Primarily Robinhood Gold subscription fees

Q1 broke down unevenly within transactions. Options revenue hit $260 million, up 8%. Equities revenue jumped 46% to $82 million. Event contracts exploded 320% to $147 million. Crypto, however, collapsed 47% to $134 million.

Net deposits totaled $17.7 billion in the quarter, an annualized growth rate of 22%.

The strategic push goes well beyond trading. Robinhood Banking has crossed $2 billion in deposits since launch with a 40% direct deposit attach rate. Retirement assets topped $27.4 billion, up 90% year over year.

In April, the U.S. Treasury named Robinhood the broker and sole initial trustee for Trump Accounts. The company also launched Robinhood Ventures Fund I, an NYSE-listed closed-end fund offering retail exposure to private companies.

Then there's Robinhood Chain, a financial-grade Ethereum Layer 2 testnet that has already processed over 100 million transactions.

Financials

Source: Stock Analysis

Robinhood's transformation since 2022 is hard to overstate. Revenue has climbed from $1.4 billion in 2022 to $4.5 billion in 2025, a trailing-twelve-month figure of $4.6 billion.

Net income swung from a $1.0 billion loss in 2022 to $1.9 billion in profit on a TTM basis. Free cash flow flipped from negative $880 million to positive $3.0 billion.

Margins tell the same story. Gross margin sits at 95.2%, operating margin at 46.3%, and FCF margin at a remarkable 65.3%.

The balance sheet carries $5.0 billion in cash with no traditional long-term debt to speak of. Q1 operating cash flow tripled to $2.0 billion versus $642 million a year ago.

Management refreshed its share repurchase authorization to $1.5 billion in March, with $250 million already deployed in Q1 at an average price near $81.

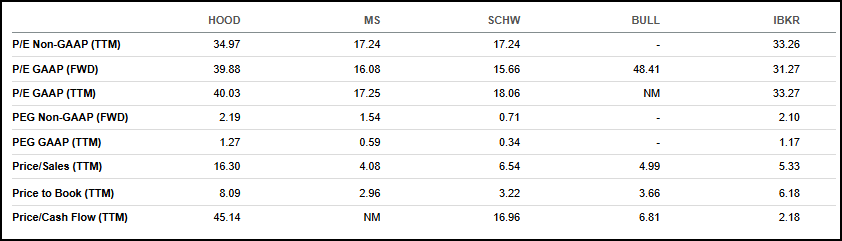

Valuation

Source: Seeking Alpha

This is where the story gets harder to defend.

Robinhood trades at 40.0x trailing earnings and 39.9x forward earnings. Morgan Stanley (MS) sits at 17.3x and Schwab (SCHW) at 18.1x. Even Interactive Brokers (IBKR), which boasts excellent fundamentals, trades at 33.3x.

The price-to-sales gap is even wider. Robinhood commands 16.3x sales while peers range from 4.1x to 6.5x.

At 45.1x price-to-cash flow, Robinhood is roughly 2.7x more expensive than Schwab on that measure.

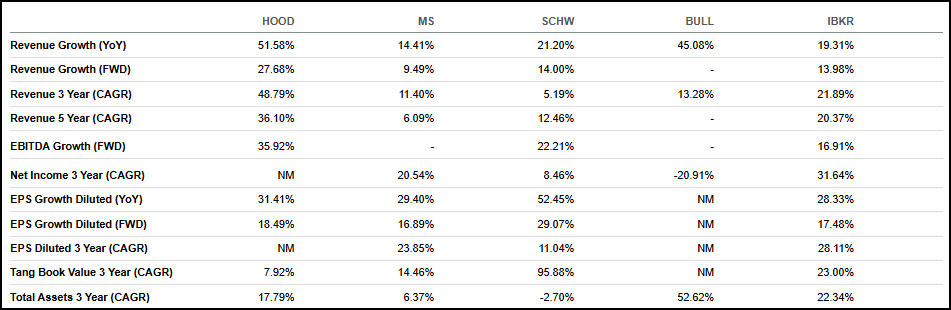

Growth

Source: Seeking Alpha

The valuation gap exists for a reason. Robinhood's 51.6% trailing revenue growth dwarfs Morgan Stanley at 14.4%, Schwab at 21.2%, and Interactive Brokers at 19.3%.

The three-year revenue CAGR of 48.8% is more than double anyone else on this list. Forward revenue growth of 27.7% still lands well ahead of every peer.

Forward EBITDA growth of 35.9% rounds out a profile no traditional broker can match.

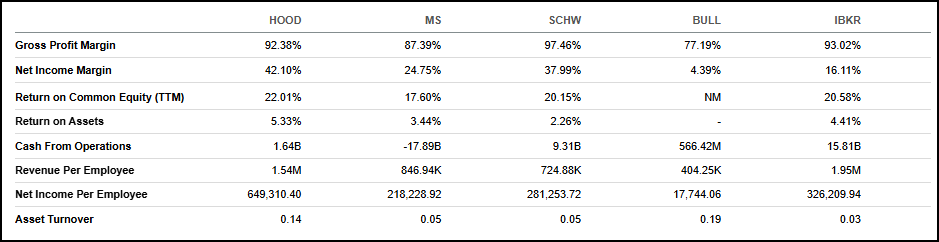

Profitability

Source: Seeking Alpha

Profitability is where the bull case earns real credit. Robinhood's 42.1% net income margin tops Schwab at 38.0% and crushes Morgan Stanley at 24.8% and Interactive Brokers at 16.1%.

Return on equity sits at 22.0%, and revenue per employee of $1.5 million reflects the operational leverage of a digital-first model.

|

![Weiss Ratings - [URGENT] Wall Street is hiding this from you](https://cdn-nl.investingchannel.com/newsletter/images/TheSpill/2026/April%202026/20260430/pexels-olly-3967020.jpg)